We would welcome your help in editing English pages on our site.

Join us.Take part in the Program.

1. Analysis … - 21. Conclusions …

1. Analysis of the facility. Profit. Cost.

Owner of the factory

(Plant) decided to sell it for personal reasons (retirement).

The Plant is in a

working condition with a positive balance, its profitability is about

6% and a net profit is approximately € 280 thousand per year.

The Plant doesn’t have any debts.

The Plant is not mortgaged or under legal

arrest.

The Plant location is quite satisfactory.

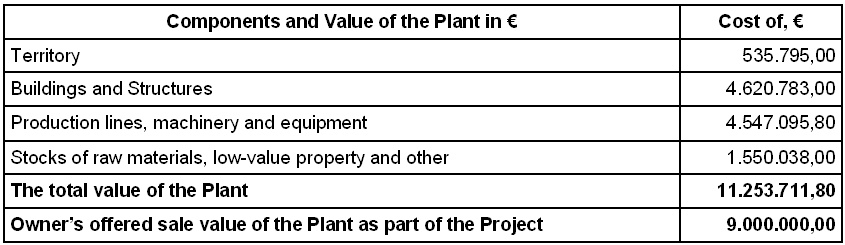

The balance value of the Plant is € 11,25

million

The net income of the Plant for 2013 was

approximately € 0,28 million (2.3% of book value).

2. Analysis of the facility.

2. Analysis of the facility.

Construction of a new

Plant with the same capacity can cost 3-4 times higher than its current balance

value.

The plant is suitable

for use as a manufacturing facility for additional products.

Type of the new

products and features of its production must be determined by properties of the

main product – patterned glass.

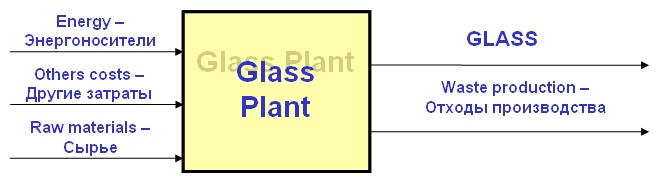

3. Diagram. Operating mode.

"Black-box” Functional diagram of the Plant

Mode of operation

Plant operating time - 7776 hours

per year (27 days per month).

Time for repair and maintenance -

864 hours per year (3 days per month).

Plant works 24 hours a day in

three shifts.

Management - 8-hour workday.

Number of employees 100.

4. Components. Value. Performance.

Performance.

The maximum capacity of the

furnace - 90 tons per day.

The average theoretical production

- 75 tons per day.

Production losses of glass (fragments)

reused in the production are about 15% (11.25 t).

5. Volume. Price. The main costs.

Average volume of

production (assumed for calculations) is 64

tons/day.

64 tones of glass is

the equivalent of

The market price of

glass - 220-270 €/t

The average price for

calculations - 245 €/t

For reference, in 2013

production reached 60 tons/day at the average

selling price of

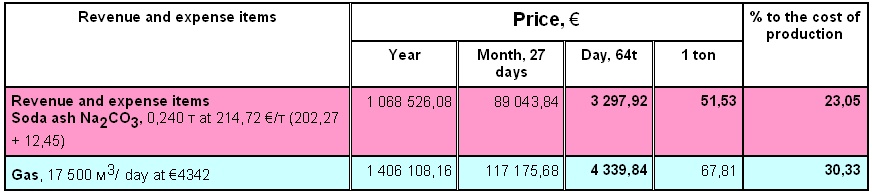

The main cost

contributors to production:

Soda ash - 23.05%;

Gas - 30.33%.

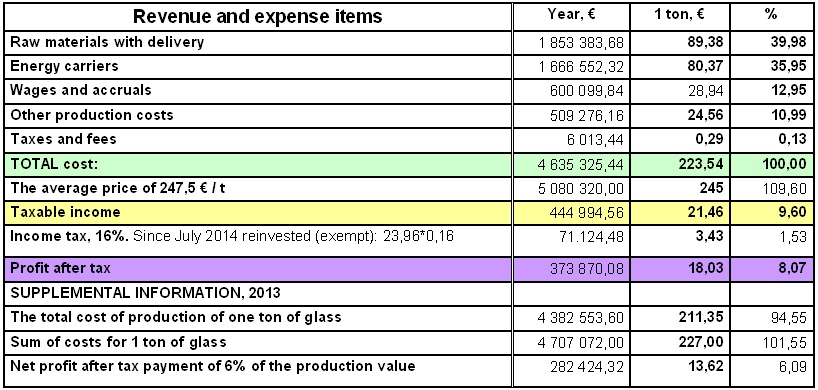

6. Structure of production costs.

7. Suppliers. Sales. Waste.

7. Suppliers. Sales. Waste.

Suppliers of raw materials are

reliable: Bega Minerale Industriale,

Uzinele Sudice-Ciech Chemical Group,

Cominex Nemetalifere, Saint Gobain Construction Products.

Suppliers of raw materials are

reliable: Bega Minerale Industriale,

Uzinele Sudice-Ciech Chemical Group,

Cominex Nemetalifere, Saint Gobain Construction Products.

Sales of products is determined by

competitive market conditions. Taking into account the development of the

region, sales have a tendency for growth.

Indicators of gaseous waste production conform to

the European standards.

The glass plant does not have

any emissions into water or to soil.

Solid waste is represented by glass

shards, which are reused in the production process.

There is no liquid waste in

production.

Environmental situation is good,

no claims to the plant’s location in the next 20 years are expected.

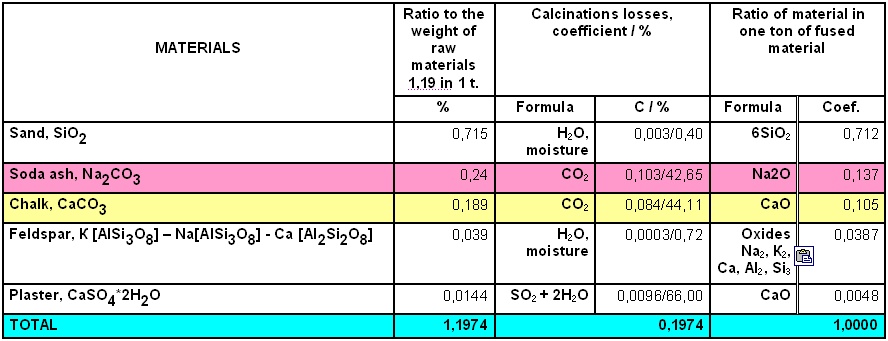

8. Loss of raw materials during calcinations.

Natural loss of raw

materials occurs due to their thermal decomposition, through exhaust with

carbon dioxide and vaporization with water.

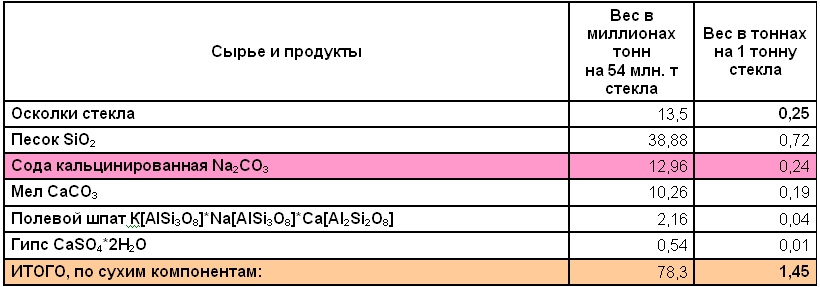

9. Gas conversions.

The combustion of

Production of 64 tons

of glass needs burning of

Incorporation of

breakdown products of soda ash Na2CO3 and CaCO3

chalk oxides into glass Na2O*CaO*6SiO2 also results in

carbon dioxide emission (Na2CO3 → Na2O + CO2;

CaCO3 → CaO + CO2).

To burn

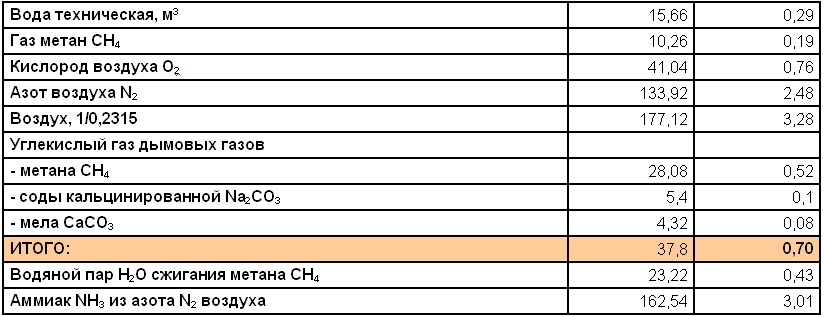

10. Nitrogen release. Conclusion on ecology.

If we consider that the oxygen

represents only 23.15% of the air used

in production, it is clear that along with steam and carbon dioxide the smoke

exhaust will contain

Conclusion about

ecology.

Despite the fact that

ecologists have no claims regarding the purity of combustion gases, it should

be noted that these gases have extremely high content of carbon dioxide. This

undoubtedly contributes to the greenhouse effect. Every ton of glass requires

3.28 tons of air, and overall 4,424 t (3.28 + 0.706 + 0.438) gas mixture (with

the addition of 0,706 t (0,186 + 0,52) CO2 and 0,438 tons (0,013 +

0,425) H2O vapor are emitted into the atmosphere.

11.

A

brief analysis of the market.

The volume of world production of

sheet glass is approximately 54 million tones per year in the amount of nearly

€21.3 billion (about 395 euro/t at the level of production).

Leading companies that

are dominating the market are: Asahi Glass Co. Ltd., Guardian Industries Corp.,

Nippon Sheet Glass Co. Ltd., and Saint-Gobain

S.A.

Technician analysts

predict the annual growth of the world market at 9,34% by 2016.

Our Plant produces

about 20 thousand tons of glass per year, or about 0.035% of the world

production.

The price on the glass

at our Plant is below the market value.

There is a tendency for

growth in this market segment.

There is a general

manufacturing opportunity in the glass market.

There is a need to

improve glass production efficiency.

12. World market. Gas emissions.

If we apply material

inputs and environmental releases calculated for our plant to global production

of sheet glass (54 million tons/year), it is possible to approximate the volume

of raw materials, carbon dioxide emissions and the nitrogen made by all plants

in the world in one year.

In total, 13 million

tons of soda (amounting approximately €2,8 billion at 215 €/t) is required for

world production of glass; it uses about 10 million tons (14.4 trillion m3) of

natural gas worth around €3,6 billion (250 €/m3 in

Transportation costs

associated with the delivery of soda ash are about 6% of its value - €168

million/year.

13. Conclusions and recommendations.

The most significant

costs for glass production - 53.38%:

- Soda ash Na2CO3, - 0,240 tons at 214,72 € / t

(202.27 + 12.45) - 23.05%;

- Gas,

Following the

principles of compatibility between economic and environmental interests we

formulate the following DIRECTIONS to modernization of the Plant.

We recommend to create

a satellite manufacturing facility dedicated to integration of glass production

into waste-free technological process in 3 steps:

1st step. Implement waste-free

self-production of soda ash.

2nd step. Utilize exhaust gases

with cleaning from sulphur compounds for production of liquefied carbon

dioxide, ammonia, fertilizers.

3-rd step. Replace methane gas

as the main energy source by using organic waste from agricultural and

municipal services, or of industrial origin.

During collection of baseline

data for the design of the 1st step, we can also evaluate the possibility of

parallel implementation of the 2nd and 3rd steps.

New production will be

located at the same premises as the existing glass Plant.

Functional diagram of

the glass production.

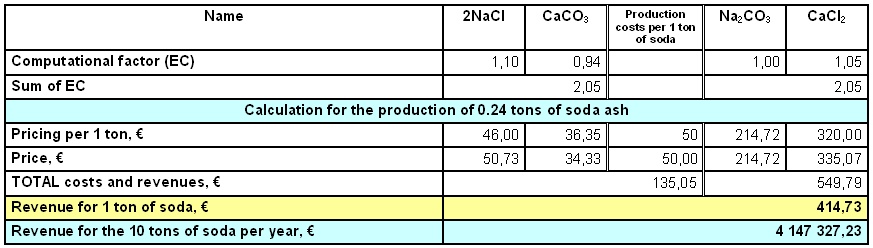

The total formula for soda ash

production process corresponds to the theoretical process 2NaCl + CaCO3

= Na2CO3 + CaCl2

Assuming estimated cost of NaCl -

46,00 € / t; CaCO3 - 36,35 € / t; Na2CO3 =

214,72 € / t; CaCl2 - 320 € / t; the costs of production (CP) at

about 50,00 € / t, then the additional revenue from the production of soda ash

for 0.24 t (replacement of purchased), 1 ton and 10 thousand tons, can be

calculated as following:

Substitution of soda

through our own production at the volume of 0.24 t per ton of glass, will

provide an additional revenue of about € 1,9 million per year, which is 5-6

times higher than the income of the current glass production. Total profit will

be about € 2,250 million per year.

The total costs for the

purchase of glass production and implementation of soda production may take

more than 10 years and is not acceptable.

To reduce the period

associated with the project costs, we need to utilize production units of soda ash Na2CO3

– at 10 thousand and calcium chloride CaCl2 – at 10,5 thousand tons

per year.

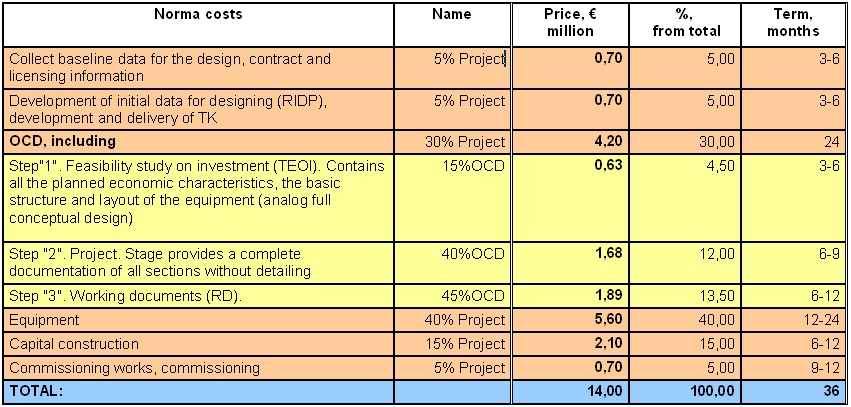

15. Project’s cost estimate.

The new production

should be about 20 million tons of marketable products per year with income of

about €4,147 million per year (€414,73)/t). This is comparable to the volume of

production of glass in terms of tonnage, but exceeds the profit from the

production of glass (€ 282-373 thousand) by more than 10 times.

Over the period of

licensing the technology for 20 years, the additional Plant revenues will total

€ 82 946 544.58.

Amount of the royalties

in the amount of 5% of the additional revenue will be € 4 147 327.23.

Manufacturing capacity

at 20 thousand tons per year corresponds to a low volume, for which the cost of

the Project is estimated at € 1,5-2 thousand per ton of installed production

capacity.

The base price for

completely new design, construction and equipment installation thus would be €

30-40 million.

Amortization of costs

after 10 years of operation, would result in writing off €3-4 million per year,

which is acceptable considering estimated earnings at €4,147,327 / Year.

Successful launch of

the new production and Project implementation

would allow to correct the basic project costs downwards.

1. For most of the

design, commissioning and construction work we plan to make use of the

south-east European labor force and local population, which would lead to the

base cost at the lower level of € 30 million.

2. Availability of

infrastructure, access roads and communications at the production site, as well

as the existing main buildings and structures reduce the design and construction costs by 1/3, and

allow to drive the base cost of the project further down to the level of € 20

million.

3. Considering that we

plan to use about 50-70% of standard equipment, and subsequent construction at

the site, the project costs can be reduced by additional 1/3 - 1/4 - to € 14

million.

Given the cost of

acquisition of the Plant in the amount of € 9 million the total for the project

costs should be estimated at € 23 million.

This number is

preliminary and tentative, and it will be further refined based on the

development of design documentation and actual expenses.

16. Crediting and earnings.

We need to harmonize

the possible use of credit lines and the potential reduction in base funding

based on the results from implementation of the project.

Reasonable time of

investment - up to 10 years.

The interest rate on

investments or loans - 5%.

We are counting on the

current Plant tax benefit on profits at 16%.

To calculate the

repayment of the project costs we assume:

- Earning from glass

production - at the level of € 0,325 million (€ 282-373 million);

- Earnings from

production of soda - at the level of € 3,94 million (€ 4,147 million minus

royalties);

- Total earnings -

about € 4,2 million (€ 4,265 million).

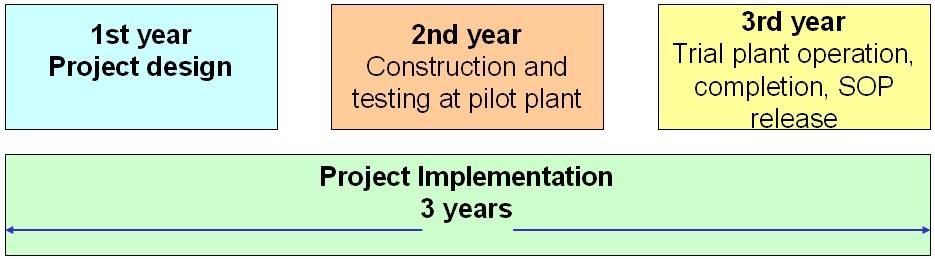

Full implementation of

our project is expected in 3 years.

3rd year – initiate

pilot operation with an additional income from soda production at € 2,000,000.

/ Year, and total earnings - € 2,3 million.

Subsequent years –

earnings € 4,2 million.

17. Production development plan.

1st year - design

2nd year – equipment construction

and testing

3rd year - trial operation,

unit completion, SOP release.

4th and subsequent

years

- operation.

18. Costs for design and implementation.

We use 3-stage design

(OCD) for the object of 4-5 degree of complexity, excluding stages for

collecting and initial data analysis, - about 30% (€ 4,5 million) costs of the

project. All steps include cost management, design supervision and licensing.

Times required to complete each step may overlap.

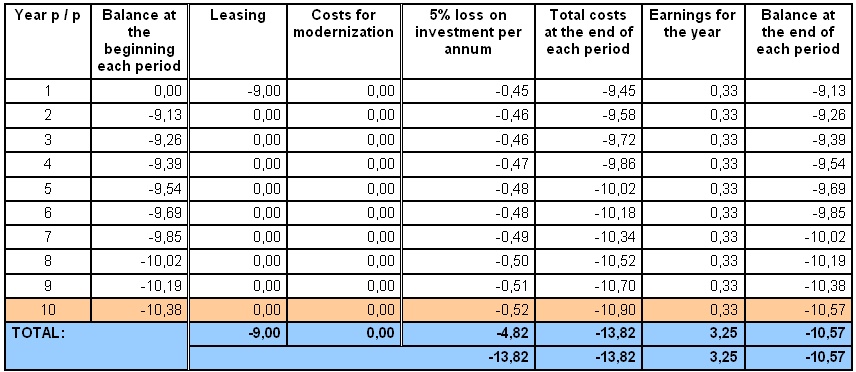

19. Return on investment without modernization.

Buying the Plant for €

9 million without modernization (in million €) can be calculated as shown in

the table.

No return on

investments, debt increase.

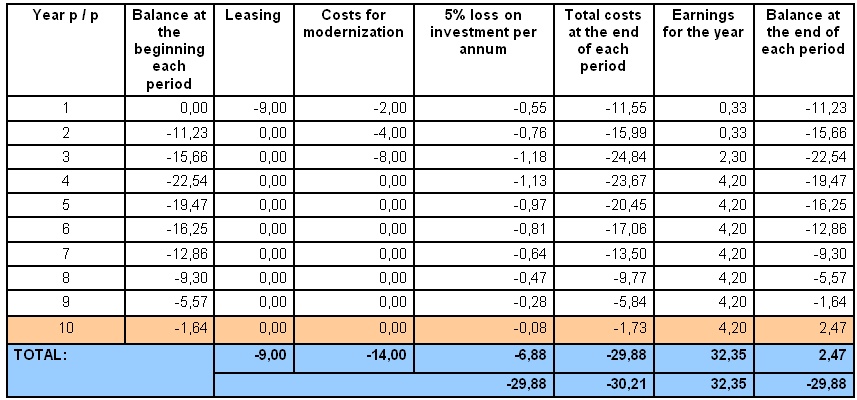

20. Return on investment with modernization.

Buying the Plant for €

9 million and proceeding with modernization through introduction of new

technology for € 14 million - the full cost of € 23 million, return on

investment is expected in 10 years as shown below.

21. Investment return analysis - conclusions.

1. The glass plant in its current

state and without modernization through introduction of new technologies has no

clear investment value and the prospect of its sale is problematic.

1. The glass plant in its current

state and without modernization through introduction of new technologies has no

clear investment value and the prospect of its sale is problematic.

The main reason - the

growing debt on invested capital – up to € 10.57 million in 10 years of service

(if plant is initially bought for € 9 million).

Furthermore, the

investment into existing glass production lines shows no economical prospect.

Co-production and sale

of by-products can be a promising proposition.

2. The volume of glass

production is 20.7 tons per year (64 tons / day * 27 days * 12 months). The

price of the Plant is € 9 million. Based on accepted cost calculations, the

construction of a new plant that would have similar capacity will require

investment of about € 30-40 million. The

return on such large investment is highly questionable. At the same time, the

current plant, at € 9 million, although with a lot of history, is quite

efficient enterprise, and has real prospects of survival and further

development when its profitability is increased.

3. There are two major

avenues to increase the profitability of the plant:

1) reduction of

production costs, production and the use of own raw materials and energy

resources;

2) the production of

by-products.

4. If we develop the

production of soda only for the needs of the plant, the efficiency of

investment will be low. It will be beneficial to introduce the production of

soda ash at capacity of 10 thousand tons and of calcium chloride at 10.5

thousand tons per year. Total production should amount to 20.5 thousand tons

per year.

5.The time needed to

collect initial data towards designing the first phase of modernization can

also be used for analysis and justification of the next steps in Plant

modernization.

Proposed version of

Plant modernization has the following advantages.

1. We can save 20% on

glass manufacturing through our own production of soda ash.

2. We can have

additional production lines that ensure revenues on excess of € 4 million per

year, which is 12 times higher than the currently earned income.

3. There are good

prospects for development of infrastructure and modernization of the company

into the 2nd and 3rd stages.

4. The company can

attract additional advertising through demonstration to the European and the

world community the new satellite glass production - the non-waste production

of soda ash; subsequent disposal of carbon dioxide and the associated

fertilizer production; and the use of new technologies to supply energy.

Join us.Take part in the Program.

We would welcome your help in editing English pages on our site.